Freight Reallocation and Industrial Network Strategy

A strategic brief on trucking constraints, intermodal adoption, and industrial location decisions

Prepared for selected clients by Kyle S. Roberts and Armando R. Tirado | May 2026

Executive Summary

The U.S. freight market is entering a structural transition, one with meaningful implications for network design, inventory positioning, and industrial location strategy. Trucking remains indispensable, but capacity is becoming harder to scale as carrier attrition, financing discipline, labor constraints, and regulation reshape the operating environment. At the same time, rail and intermodal networks are reemerging as key transit modes across a broader share of freight. For customers evaluating long-duration footprint decisions, that shift matters because it changes which locations and network configurations may prove most resilient and durable over time.

In 2019, the American Trucking Associations identified a significant structural driver shortfall and projected that the gap could widen materially over time (Costello, Truck Driver Shortage Analysis 2019, 2019). While the timing and magnitude have not unfolded in a straight line, the underlying thesis remains relevant: the trucking market is becoming more complex under simultaneous pressure from labor availability, equipment economics, lender caution, and broader supply chain volatility influenced by macroeconomic and geopolitical issues. The COVID-19 period made that complexity impossible to ignore, first through extreme tightness and then through historic overcapacity. By late 2025 and early 2026, however, market signals increasingly pointed to a different dynamic: tightening conditions driven less by a surge in freight demand than by a shrinking and more selective carrier supply base.

Our working view is that the market is moving toward a more deliberate allocation of trucking capacity, with rail and intermodal absorbing more line-haul volume where feasible and trucking concentrating more of its value in shorter, faster, and higher-priority moves. As contract freight becomes more valuable and local or less predictable moves absorb more volatility, transportation economics begin to influence site selection more directly. If that proves directionally correct, it will become increasingly important for customers to evaluate transportation optionality alongside the regulatory environment, labor, occupancy cost, and proximity to demand. This influence is particularly acute when decision making about Import North American freight.

The Market Thesis

The clearest signal in domestic freight today is not simply that more goods are moving, but that the most efficient way to move them is changing. Freight volume is relatively flat; this is fundamentally a story of modal allocation rather than pure demand growth. Rail and intermodal networks are becoming more relevant not only because they can lower costs – in some instances up to 50% (RSI Logistics, 2024), but because they can also relieve pressure on a trucking market showing growing signs persistent of structural tightness. As supply chains begin optimizing for resilience and durability rather than transit speed alone, the competitive map starts to shift. That shift is especially relevant as freight flows into the United States continue to evolve, particularly from North and South American trade partners.

That matters because rail is no longer confined to the longest or least flexible freight movements. Across established corridors, intermodal service is becoming more capable, more integrated, and more relevant to shippers managing volatility. Transload infrastructure has also become more accessible and visible, with industry directories and operating platforms making it easier to identify facilities, compare capabilities, and design truck-rail combinations with greater precision. At the same time, digital rail tools are improving network transparency. CedarAI, a Seattle-based rail technology company, is one example of a platform offering shippers greater real-time visibility into rail movements, equipment status, and related handoffs. The broader implication is that multi-modal optionality is becoming more practical – and more scalable – than it was in prior freight cycles, affording shippers and BCO’s the visibility on inventory in motion and during modal shift.

Even where adoption is uneven, the direction is clear: if line-haul freight can be shifted onto more stable rail networks with significant cost and emissions savings, then scarce trucking capacity can be redirected to the segments where it creates the most operational value. That is a meaningful strategic change for logistics planning, inventory positioning, and industrial site selection, which has been enabled by off-the-shelf technology and railroad infrastructure investments.

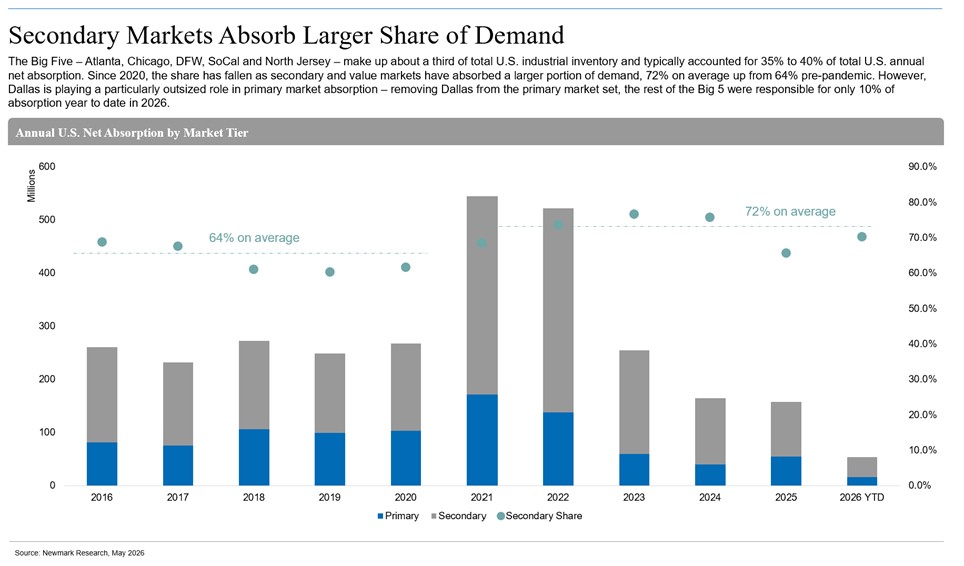

U.S. Annual Net Absorption by Market Tier. Lisa DeNight – Newmark 2026.

What Is Driving the Shift

The trucking market has spent the last several years in a prolonged shakeout. The collapse of Yellow Corp. in 2023 removed a major LTL player from the system, and subsequent carrier exits and bankruptcies have highlighted how fragile carrier economics remain. More broadly, recent industry reporting points to persistent stress across both large and small operators, with tariffs, debt burdens, overinvestment in equipment during the pandemic-era freight boom – much of which is subjective to obsolescence due to regulation – which causes further need to invest, and weak rate environments all contributing to continued failures. Yellow Corp. remains the clearest headline example, but the broader significance lies in the cumulative effect: tighter capacity, more selective carrier behavior, and a market increasingly shaped by stubbornly difficult to correct supply-side contraction rather than broad demand acceleration.

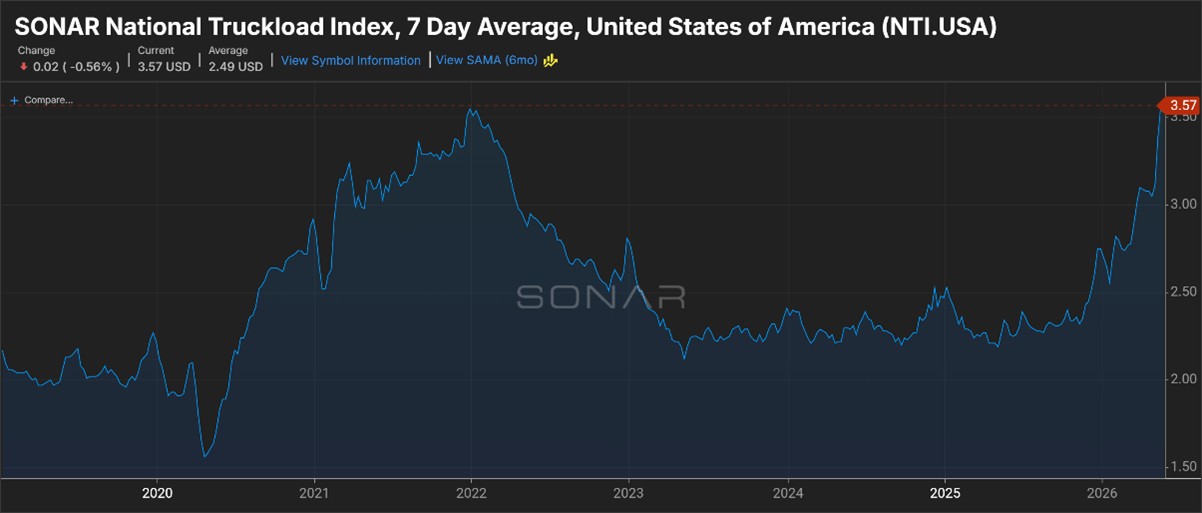

National Average price-per-mile shows increasing freight costs. The start in this rise started at the end of Q3 2025, several months before the conflict in Iran. Graph provided from Sonar© 2026.

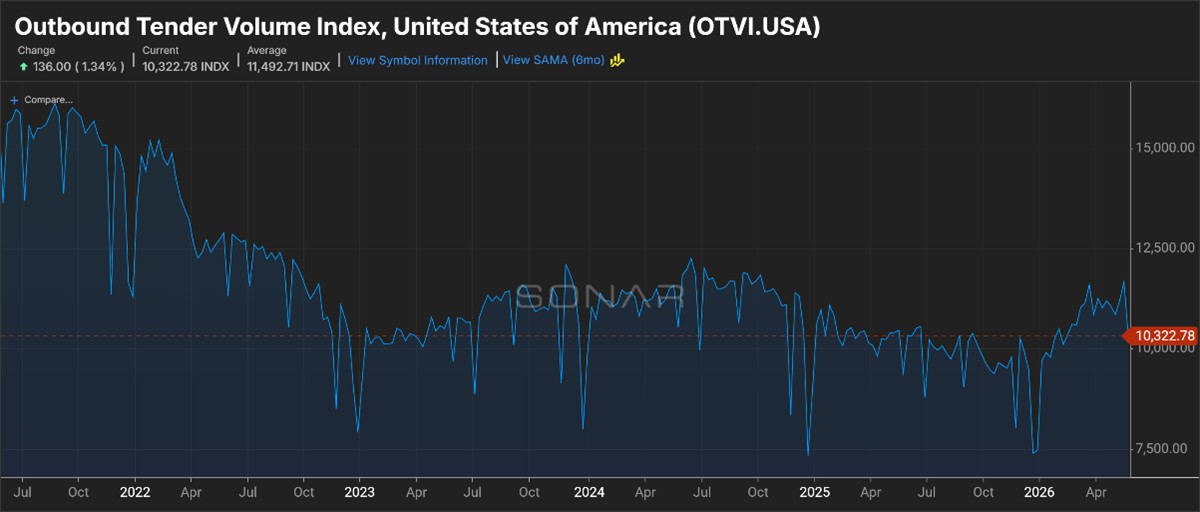

Outbound tender volume is a direct reflection of freight demand. As the 5-year outlook shows, demand is relatively stable and far below the levels experienced in 2021. Graph provided from Sonar© 2026.

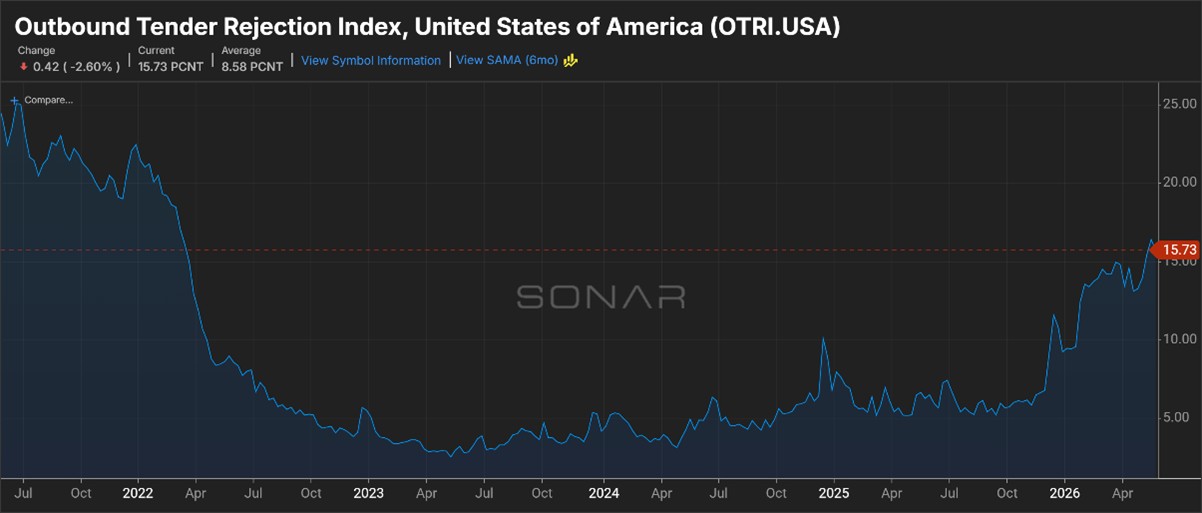

Tender rejection rates have been increasing since July 2025. Tender rejection rates are a direct capacity indicator. Graph provided from Sonar© 2026.

At the same time, fleets are contending with higher replacement costs, regulatory uncertainty, and more difficult operating conditions. California Air Resource Boad; Zero- Emissions, and clean idle trucking policies continue to shape procurement decisions for vehicles which are or may operate in the state and has also become a policy model for other jurisdictions, even as the related Advanced Clean Fleets regime was narrowed for many private fleets after CARB did not secure a federal waiver (Warness, 2024). The practical implication is not a single uniform cost shock, but a more complicated replacement environment in which fleets face higher capital requirements, narrower equipment choices, and more cautious deployment decisions in affected markets. Combined with weaker credit conditions and tractor sales that remain below expansionary levels but at significantly higher cost, those factors make the trucking market harder to scale quickly, especially at the margin.

A further constraint comes from recent federal enforcement and licensing changes affecting driver qualification. In April 2025, the Trump administration directed the Federal Motor Carrier Safety Administration to restore stricter English-language proficiency enforcement for commercial drivers, and by June 25, 2025, English-language violations again became an out-of-service condition during roadside inspections. The FMCSA also moved in late 2025 and early 2026 to tighten eligibility for non-domiciled CDLs, narrowing the pool of foreign-domiciled drivers who can qualify or renew. Based on our research, these combined changes could reduce the effective CDL driver pool by roughly 10 percent, further tightening capacity in a market that is already becoming harder to scale (Lockie, 2025).

Those pressures feed directly into pricing. As available capacity tightens, contract freight becomes more valuable, spot markets grow more volatile, and shippers increasingly pay for certainty. Current market reporting suggests that 2026 tightening is being driven primarily by carrier exits and constrained capacity rather than a dramatic rebound in freight demand, with spot rates and tender rejections rising faster than contract pricing in several periods. In practice, that tends to push the greatest volatility into shorter-haul, local, and less predictable freight while larger shippers move quickly to secure committed capacity. In that environment, transportation is no longer a background assumption in network design; it is becoming a primary strategic variable.

Global supply chain volatility has reinforced this shift. Disruptions in the Red Sea during 2023 and 2024 and in the Strait of Hormuz in 2026 have increased freight, fuel, insurance, and inventory risk across portions of major trade lanes. When routing becomes less predictable, companies respond by carrying more inventory, diversifying network nodes, and prioritizing resilience over pure efficiency. That response supports not only transportation demand, but also warehousing, transloading, and third-party logistics activity closer to destination markets. In many respects, this is the inverse of the pattern that once favored secondary and tertiary markets, where lower occupancy costs were sufficient to offset higher transportation costs. That tradeoff is becoming less compelling as freight expense and service risk rise relative to pure occupancy-cost savings.

Taken together, these forces point to a simple conclusion: the next freight cycle will be defined less by a broad surge in goods movement than by a reallocation of network value. Transportation cost and service reliability are beginning to matter more relative to pure occupancy-cost arbitrage, especially where freight must move quickly or consistently into major demand centers especially in hyper-competitive segments such as e-tail/retail. The likely winners will be the operators, corridors, and markets that can offer optionality across truck, rail, and inventory positioning, rather than simply the lowest nominal occupancy cost.

One important distinction is that rising fuel costs, while widely cited as a source of pressure on freight carriers, do not affect every operator equally. Higher fuel prices do raise costs across manufacturing and distribution which can impact volume, but most carriers are relatively insulated at the operating level. The majority of rail and truck carriers have fuel surcharge escalators built into their contracts, and spot rates generally incorporate current fuel prices as well. On average, fuel represents roughly 20 to 30 percent of a trucking carrier’s operating costs, while equipment and labor typically account for a larger share (datatruck, 2025). Where fuel can become more disruptive is among smaller trucking firms or operators without the liquidity to bridge the period between fuel purchase and load payment, particularly in an industry where payment terms of 90 days or more are not uncommon.

What It Means for Industrial Real Estate

If transportation becomes less cheap, less flexible, and less predictable, industrial demand will increasingly follow network logic which changes based upon variable shift in transportation costs as other variables remain relatively stable. We saw early versions of this during the COVID period, when occupiers favored population-centric markets and deeper inventory positions to protect service levels. That same logic may return in a more durable form. Facilities closer to end demand, labor pools, and established freight corridors should become more strategic as delivery commitments tighten, local dray and short-haul costs become more volatile, and replenishment risk carries greater weight. This shift may also place greater emphasis on population growth trends when evaluating market selection.

At the same time, intermodal and transload infrastructure have become a more meaningful differentiator across markets. As end-users recognize modal accessibility and benefits, locations with modern rail connectivity, available inland capacity, and the ability to shift efficiently between modes are better positioned to capture redistributed freight flows. Conversely, some markets that benefited primarily from low occupancy cost relative to transportation expense may face a more difficult value proposition if line-haul and local freight costs remain elevated or less predictable. If that thesis holds, the next wave of industrial demand may favor markets that combine population access with modal flexibility, rather than those that competed primarily on low occupancy cost alone.

This is why freight strategy and real estate strategy can no longer be binary with OTR freight movements if durability increases and service levels are static and/or improve. Landed cost, service reliability, and inventory placement are converging into a single decision framework. For developers, investors, and occupiers, the strategic question is no longer just a race to the bottom of occupancy cost; it is where a network can remain resilient when transportation markets tighten.

What This May Mean for Clients

The central implication of this brief is not that trucking is losing relevance. It is that freight economics may be evolving in ways that could reshape how tenants and shippers evaluate network durability over the next several years. If trucking capacity remains constrained at the margin while rail and intermodal continue improving across viable corridors, industrial decisions may increasingly favor locations that combine market access with transportation flexibility, shorter-term adaptability, and service resilience.

For our clients, three considerations stand out. First, transportation optionality may warrant greater weight in long-range site evaluation, particularly where service commitments depend on reliable access to both line-haul and local capacity. Second, markets with credible intermodal, rail, and transload infrastructure may deserve closer attention as freight flows rebalance and occupiers seek more predictable delivery schedules and landed costs. Third, network strategy, inventory positioning, lease flexibility, and real estate strategy should be evaluated together with increased emphasis on network durability and predictable network costs than has been the case in recent cycles.

In summary, one potential implication of this shift is greater interest in autonomous transportation and other technologies that can improve network efficiency as labor and capacity constraints persist. Any large-scale adoption, however, would still depend on the supporting power infrastructure, including generation, storage, and grid capacity. More broadly, these trends may encourage continued modal shift and fuller utilization of supply chain assets, which could further influence how occupiers evaluate space, throughput, and network design. At the same time, many of these potential growth opportunities are highly capital intensive. In an environment where capital increasingly favors durability and disciplined underwriting, financing some of the required investments may prove more challenging than in prior periods when capital was more readily available.

It is not difficult to envision a return to networks built around large national or super-regional distribution centers that can rapidly deploy inventory to smaller, more nimble distribution and fulfillment facilities. Such models improve the ability to respond to fluctuations in market demand while also increasing network durability. In some respects, Amazon’s network evolution appears broadly consistent with this direction, while also reflecting deeper integration across freight, retail, and distribution functions. That kind of vertical integration and supply chain diversification is not without precedent; in some ways, it resembles elements of the manufacturing and logistics landscape that existed before China’s rise as a dominant global trade platform following most-favored-nation treatment and entry into the World Trade Organization.

For clients, the implication is clear: transportation is no longer a background assumption in site selection; it is becoming a primary determinant of long-term network performance. The most durable decisions will likely come from aligning real estate strategy with freight optionality, service resilience, and the ability to adapt as market conditions continue to shift.

Sources

Costello, B. (2019). Truck Driver Shortage Analysis 2019. Washington D.C.: American Trucking Association.

Costello, B. (2019, July). www.trucking.org. Retrieved from American Trucking Association: https://www.trucking.org/sites/default/files/2020-01/ATAs%20Driver%20Shortage%20Report%202019%20with%20cover.pdf

datatruck. (2025, July 17). The Real Costs of Running a Trucking Company in the USA: a Carrier’s Perspective. Retrieved from www.datatruck.com: https://www.datatruck.io/blog/the-real-costs-of-running-a-trucking-company-in-the-usa%3A-a-carrier’s-perspective

Lockie, A. (2025, September 26). DOT Hopes to Force 194,000 Non-Domiciled CDL Holders Out of Trucking . Retrieved from www.overdriveonline.com: https://www.overdriveonline.com/regulations/article/15767991/fmcsa-to-force-nearly-200k-nondomiciled-cdl-holders-out-of-trucking?utm_source=copilot.com

Warness, L. (2024). California Air Resouce Board, Advanced Clean Fleet and Clean Truck Rules. Washington D.C.: Forest Resources Association.

Appendix: Glossary of Terms and Acronyms

This appendix defines selected terms and acronyms used in this brief that may be unfamiliar to a general audience.

3PL (Third-Party Logistics): A company that provides logistics services for other businesses, such as transportation management, warehousing, inventory handling, or freight coordination.

Autonomous Transportation: Transportation systems that use automated or self-driving technology to move goods with less direct human control.

End-Market Adjacency: Proximity to the final customer market or demand center that a facility is intended to serve.

Intermodal: Freight transportation that uses more than one mode of transport, such as rail and truck, within a single shipment journey.

CDL (Commercial Driver’s License): A license required to operate certain large or specialized commercial motor vehicles, including heavy trucks and some vehicles carrying hazardous materials or passengers.

CLP (Commercial Learner’s Permit): A permit that allows a person to practice operating a commercial motor vehicle under qualified supervision before obtaining a full CDL.

Landed Cost: The total cost of getting a product to its destination, including transportation, storage, duties, handling, and other related expenses.

FTL (Full Truckload): A trucking service in which a shipment uses most or all of a trailer’s capacity and typically moves directly from origin to destination without being combined with other shippers’ freight.

Line-Haul: The long-distance portion of a freight movement between major origin and destination points, usually before local pickup or final delivery.

LTL (Less-Than-Truckload): A trucking service for shipments that do not fill an entire trailer and are combined with freight from other shippers.

Modal Shift: A change in how freight is moved from one transportation mode to another, such as from truck to rail.

Occupancy Cost: The cost of using a facility, including rent and other operating expenses associated with the space.

Optionality: The ability to choose among multiple operational or network alternatives as conditions change.

Spot Market: The market for freight purchased on short notice at current market rates rather than under a longer-term contract.

Supply-Side Contraction: A reduction in available market capacity or supply, such as when carriers exit the market or reduce service.

Throughput: The volume of goods a facility or network can handle over a given period of time.

Transload / Transloading: The process of moving goods from one mode of transportation to another, such as from rail to truck, usually at a transfer facility.