Supply Chain as a Competitive Advantage

Executive Summary

Modern regional competitiveness is no longer defined by incentives, branding, or aspirational industry targeting- it is defined by supply chains. As the paper notes, “competitiveness depends on the ability to bring inputs‑in and move outputs‑out as efficiently, consistently, and affordably as possible”. Regions that understand this reality, and invest accordingly, are the ones positioned to win in today’s economy.

This analysis traces how U.S. supply chains evolved from Roman‑style logistics principles to rail‑driven industrialization, containerization, globalization, and now nearshoring. The pandemic exposed the fragility of long, offshore‑dependent networks, where Forty-Foot-Equivalent-Unit (FEU) rates from Shanghai to Long Beach spiked 500% and inventory sat idle in transit. These shocks accelerated a structural shift toward resilience, regionalization, and shorter, more controllable supply chains. Mexico’s rise as the United States’ largest import source – shipping $510 billion in goods in 2024 – illustrates this realignment and the growing strategic value of North American multimodal networks.

For communities, the implication is clear: stop chasing marquee industries and start evaluating true competitive advantage. As this paper emphasizes, “manufacturing success depends on whether a region can bring inputs in and move outputs out efficiently”. Transportation cost, capacity balance, and modal optionality now outweigh traditional cost drivers such as labor or real estate.

Utah’s case study demonstrates both the challenge and the opportunity. The state benefits from a central location, strong workforce, and a robust defense industrial base, yet lacks depth in rail‑served industrial land, cold‑chain/Good Manufacturing Practices (GMP) capacity, and tier‑2/3 feedstock suppliers. Much of Utah’s raw material wealth – such as copper cathode – exits the state for value‑added processing elsewhere. A shortened, Utah‑based supply chain could reverse this dynamic, closing critical feedstock gaps, strengthening advanced manufacturing, and capturing value currently lost to other regions.

This paper’s core message is unambiguous: supply chains are the strategy. Regions that align economic development with the realities of goods movement will shape their own futures; those that do not will be shaped by the decisions of others.

Supply Chains as Strategy: Rethinking Regional Competitiveness in the Modern Economy

We often hear elected officials, community leaders, and economic development professionals’ express ambitions to attract specific industries or marquee companies to their regions. Buzzwords like advanced manufacturing, biotechnology, rare earth elements, and critical minerals are frequently invoked. They make compelling soundbites at groundbreaking events or on the campaign trail – but how often do these stakeholders fully understand what those industries require? And more importantly, is it even viable to manufacture those products in the markets they are promoting?

While there are always exceptions, the supply chain is often the first place to examine in a manufacturing ‑ or distribution‑dependent business. Does the region provide a genuine competitive advantage for that firm, or is it more efficient to produce the item in another market? If the answer to either question is no – or even uncertain – then deeper due diligence is essential to identify which market conditions would turn those answers into yes. Manufacturers and distribution organizations frequently rely on site selectors to provide these insights, yet the same tools and thinking are not consistently applied within governmental economic development efforts.

Healthy and successful manufacturing and distribution ecosystems depend on a careful balance of population density, robust multimodal transportation networks, a workforce with the right technical skills, and sufficient industrial real estate to support clustered, symbiotic suppliers. As we enter the automated age of warehousing and distribution, reliable power generation and transmission have become equally essential determinants of regional competitiveness. In today’s industrial environment, it is not uncommon for a 1,000,000‑square‑foot distribution or light‑manufacturing facility to require more than 40 megawatts of available power – roughly eight times the demand seen just five years ago. Understanding the nexus between power and transportation is now critical, as the two are increasingly intertwined drivers of industrial viability.

At the most fundamental level, competitiveness depends on the ability to bring inputs-in and move outputs-out as efficiently, consistently, and affordably as possible, with minimal exposure to external risks such as environmental disruptions, resource constraints, or geopolitical instability. This principle applies across the board – from power generation to the production of advanced military‑grade technologies. Supply distribution ultimately aligns with where product demand is concentrated and which transportation modes can serve that demand most efficiently. As a result, “make where you sell” environments tend to flourish, often at a pace that outstrips traditional market expectations.

In this analysis, we will examine current and historic U.S. supply chains, trace the evolution of goods movement, and explore how strategic development can be leveraged into a competitive advantage. Understanding this context is essential for any region seeking to position itself as a credible destination for modern manufacturing and distribution.

The Historical Foundations of America’s Supply Chain

The foundations of modern supply chain management can be traced back to the Roman Empire. Under Roman direction, an extensive network of roads, ports, and sea lanes connected Europe, North Africa, and the Middle East, enabling the movement of goods at a scale unprecedented for the ancient world. Granaries, warehouses, and depots were strategically positioned to prevent shortages, and Rome relied on buffer stocks and regional storage – early precursors to today’s distribution centers. Standardized weights, measures, and packaging (such as amphorae) supported predictable trade flows, while sophisticated record‑keeping and taxation systems ensured administrative consistency. To sustain the Roman military machine, merchants and contractors moved goods under state contracts, forming one of the earliest examples of outsourced logistics.

This framework shaped how much of the developed world moved goods until the mid‑19th century, when the first modernized railroads emerged in England. Rail transport introduced unprecedented speed, reliability, and scalability, and the model quickly spread throughout the British Empire and into the “New World.” In the United States, however, early supply chains remained predominantly maritime due to vast distances, low population density, and the lack of a standardized road system.

As with the Romans, the English brought a degree of standardization across their empire, including a uniform rail gauge – the distance between the rails – set at 56½ inches, a standard that remains in place today. This consistency allowed equipment to move freely across interconnected networks without needing to be changed out. The resulting scalability helped fuel the Industrial Revolution: iron, coal, and other critical feedstocks could now be transported at far greater speed and volume, accelerating industrial growth and enabling modernization at an unprecedented pace.

Although roads existed in the United States, they lacked uniform construction, oversight, and connectivity well into the early 20th century. As settlement pushed westward, much of the interior was linked only by a patchwork of wagon trails. A cross‑country journey in the 1840s or 1850s could take five to seven months and carried significant risks – both to travelers and to the goods they carried.

While rudimentary rail experiments appeared in the early 1800s, modern railroading in the United States began in 1827 with the charter of the Baltimore & Ohio Railroad (B&O). This launched a century‑long railroad boom that reshaped the nation’s economic geography.

The completion of the Transcontinental Railroad in 1869 marked a pivotal turning point: goods could now move across the country at scale, and a journey that once required months could be completed in seven to ten days by the 1870s. Railroads connected communities and markets that had previously been isolated, and the network continued to expand, reaching peak freight output during the Second World War. World War II also marked the emergence of sustained multimodal transport systems on a global scale, cementing this strategy in modern logistics culture.

The introduction of the internal combustion engine at the turn of the 20th century added a new dimension to freight movement. By the 1910s, early tractor‑trailers were hauling goods across the country’s fragmented road system, laying the groundwork for the modern trucking industry that would eventually complement – and compete with – the railroads.

In 1926, the United States established its first national road network with the creation of the U.S. Numbered Highway System. Routes such as US 1, US 30, and US 40 connected much of the Eastern Seaboard and extended westward, enabling more reliable long‑distance overland travel. This marked a meaningful shift toward a multimodal supply chain: goods manufactured in the industrial East could now reach growing populations in the Midwest and West with greater consistency and speed.

Under President Franklin D. Roosevelt’s New Deal, tens of thousands of additional roads were built or improved, further stitching the nation together. This momentum accelerated after the passage of the Federal Aid Highway Act of 1956, which created the Interstate Highway System and transformed national freight mobility.

Another major shift in freight flows emerged with the rise of commercial air travel beginning in the 1930s. The introduction of jet‑powered aircraft in the postwar era compressed cross‑country travel times from months in the 1860s to mere hours within a single century. These developments strengthened the national supply chain and positioned the United States as the epicenter of global manufacturing and distribution in the postwar era, pushing finished goods to markets around the world.

In the 25 years following the end of the Second World War, a significant shift began to take shape. A recovering global economy, a decades‑long Cold War with the Soviet Union, the end of widespread colonization – which created a wave of newly independent nations – and increasing dependence on Middle Eastern oil all contributed to the emergence of large‑scale globalization and a reshaping of the U.S. economic landscape. By 1976, the United States became a net importer of goods for the first time, marking a structural turning point in how the nation sourced and consumed products.

While domestic transportation networks continued to mature, a new force began reshaping global freight flows: the standardization of international shipping. The advent of containerization in the late 1950s and its rapid adoption through the 1960s and 1970s fundamentally restructured how goods moved into, out of, and across the United States. Combined with shifting patterns of global manufacturing, this innovation set the stage for the modern, port‑centric supply chain and the inland distribution networks that followed.

The Making—and Unraveling—of East to West Freight Flows

In the years leading up to China’s 2001 accession to the World Trade Organization (WTO), North American supply chains had already begun reshaping themselves. The single most consequential catalyst for this trajectory was the series of U.S. – China trade agreements initiated in the early 1970s. A handshake in February 1972 between President Richard Nixon and Chairman Mao Zedong ended nearly 25 years of geopolitical tension and opened the door to economic engagement across East Asia. By 1980, China had secured most‑favored‑nation status, solidifying its position as a critical U.S. trade partner. By 1995, U.S. imports from Asia reached $131.2 billion, compared with $59.3 billion in exports.

As global trade accelerated, significant infrastructure investments throughout the 1990s and early 2000s expanded the capacity of U.S. freight networks, pushing international cargo inland to regional and national distribution centers. The Mississippi River corridor—along with the I‑35 and I‑55 corridors – emerged as major distribution hubs due to their population densities, multimodal connectivity, and deep industrial real estate bases. Regions that had historically anchored U.S. manufacturing increasingly shifted toward distribution as production moved offshore. Transit times from Shanghai to Chicago routinely fell below 30 days, reinforcing the competitiveness of inland distribution networks. As a result, just‑in‑time supply chains built around Asian‑sourced products became both practical and reliable, reaching their peak at the end of 2019, just before the onset of the COVID‑19 pandemic.

During this period, import flows entered U.S. ports on both the East and West Coasts before moving into distribution centers along the Mississippi corridor, where goods were warehoused and dispatched to consumers. The rapid rise of e‑commerce further entrenched this model, accelerating demand for high‑velocity fulfillment networks and deepening reliance on inland hubs.

To accommodate this surge, supply chains evolved dramatically over the last 30 years. West Coast ports reached unprecedented volumes in the mid‑2000s, with the Los Angeles/Long Beach complex ranking among the world’s top ten container ports – and the largest outside Asia – between 2004 and 2010 (The Port of Los Angeles, 2026). While early growth in U.S. trade was heavily concentrated in China, import sourcing diversified over time to include Vietnam, Japan, South Korea, and other Asian economies. Despite rhetoric surrounding tariffs in recent years, U.S. import traffic from Asia reached an all‑time high in 2025, with $1.416 trillion in imports and $598.8 billion in exports.

On January 23, 2020, Chinese authorities locked down the city of Wuhan and much of Hubei Province in response to an emerging virus. What began as a regional health emergency quickly cascaded into widespread manufacturing and supply chain disruptions across China. By mid‑March 2020, the virus had reached U.S. shores, shutting down industry and triggering a global pandemic. In a highly interconnected global economy, the impact was unprecedented. Transportation flows and asset cycles fell out of balance, disrupting the movement of goods ranging from necessities – toilet paper and baby formula – to critical technologies and healthcare supplies.

Through this period, organizational supply chains were exposed for what they had quietly become: fragile, lean, and highly sensitive to disruption. Networks strained under backlogs, and essential inventory sat idle in transit. Costs surged. Spot rates for a forty‑foot equivalent unit (FEU) from Shanghai to Long Beach climbed from roughly $2,500 to more than $15,000 per container – a 500% increase (UNCTAD, 2021).

As organizations spent exorbitant amounts on transportation, both consumers and producers suffered in parallel. The cost to manufacture and deliver goods began outpacing both willingness – and increasingly the ability – to pay. U.S. non‑housing debt rose from $4.2 trillion in Q1 2020 to $5.17 trillion by Q4 2025, a 23.1% increase (Federal Reseve Band of New York, 2026). Over that same period, the U.S. population grew only 3.1% (US Census Bureau , 2026), underscoring how sharply household financial burdens escalated relative to demographic growth. Median wages rose just 21.5% over the same period, highlighting how supply‑chain‑driven inflation outpaced earning power (Maryland Department of Planning, 2026). FEU spot rates at the end of Q4 2024, while significantly cooled from their pandemic peak, remained well above pre‑pandemic levels at roughly $4,800 – a 92% increase driven largely by geopolitical disruptions. Through 2025, rates continued to decline and moved closer to pre‑pandemic norms, reinforcing the broader story of U.S. inflation flattening and the subsequent interest‑rate cuts we observed.

With these pressures reshaping the landscape of U.S. commerce, a structural economic shift became unavoidable. The lasting impact of an increasingly interconnected web of global risks – where multiple disruptions can be triggered simultaneously or in rapid succession – has elevated resilience from a strategic priority to an operational necessity. Post‑pandemic geopolitical conflicts have added new volatility to traditional shipping routes, driving further disruption and cost escalation. As a result, reliability across multimodal transportation networks has become a central focus, particularly within long‑established lanes now exposed to this global web of interdependent vulnerabilities. The conflict between Iran, Israel, and the United States that erupted in February 2026 underscores this reality: a disruption to a strategic ocean corridor – one representing just 0.003% of the world’s ocean area – drove shipping and global fuel costs up more than 40% and constrained production of petroleum‑adjacent feedstocks. The ripple effects have made goods ranging from hospital PPE to plastics increasingly difficult to source. Any product that relies on global transport has been affected – an impact radius far exceeding the nations directly involved in the conflict.

Mexico’s Emergence as a Dominant U.S. Import Source

While Asia was capturing global attention as the dominant force in international trade, Mexico was quietly building an industrial powerhouse of its own. With the passage of North-American-Free-Trade-Agreement (NAFTA) in 1994 – and later the United-States-Mexico-Canada-Agreement (USMCA) – a new competitive landscape emerged: one with minimal tariff barriers and many of the same cost advantages as Asia, but with dramatically shorter supply‑chain lead times and fewer risk vectors. At the same time, Mexico strengthened physical security around key infrastructure and invested heavily in expanding network capacity, laying the groundwork for large‑scale manufacturing growth.

In April 2024, Canadian Pacific Railway merged with Kansas City Southern to form CPKC, creating North America’s first and only single‑line railroad connecting Canada, the United States, and Mexico. CPKC now markets service from San Luis Potosí to Chicago in under 98 hours, with no interchanges required. The merger sparked a wave of competitive responses, as other U.S. Class I railroads formed alliances to replicate this level of cross‑border fluidity. By the end of 2024, the newly formed railroad had completed a second bridge across the Rio Grande in Laredo – where roughly half of all U.S. rail freight border crossings occur – effectively doubling operating capacity.

Historically, more than 80% of goods in Mexico have moved by truck. Today, streamlined cross‑border rail networks—combined with accelerating nearshoring momentum – are positioning rail to absorb the next wave of industrial growth and provide the capacity required for a modern North American supply chain.

By the end of 2024, the Tren Maya was completed, connecting the 1,554‑km Yucatán Peninsula by rail. While primarily a passenger system, it establishes the foundational infrastructure for future freight alternatives that could eventually bypass the Panama Canal and support new manufacturing activity in the region, further strengthening supply‑chain resilience.

Following the pandemic‑era supply‑chain disruptions, Mexico attracted $173.18 billion in foreign direct investment into manufacturing between 2020 and 2024 (MacroTrends, 2026). This surge in investment has contributed to a clear modal and geographic shift in North American trade. In 2024, Mexico surpassed China as the largest source of U.S. imports, shipping $510 billion in goods—representing 16% of all U.S. imports. China followed with $463 billion (14%), and Canada ranked third with $421 billion (13%) (Trading Economics, 2026).

An important trend to watch is the rise of Mexico’s deep‑water ports as legitimate freight hubs. The Port of Manzanillo now ranks among the top ten North American ports by container volume, and its planned $3 billion USD expansion will double capacity to 10 million TEUs by 2030 (Delgado, 2025). From 2015 to 2024, Asia‑to‑Mexico import values increased by 90%, and Mexico’s containerized rail traffic grew by 22%—clear indicators of shifting trade flows and strengthening port‑rail connectivity.

To further underscore the modal shift underway, US international intermodal volumes declined 2.6% in Q1 2026 compared to Q1 2025, while domestic intermodal increased 3.6% over the same period. As Mexican ports emerge as North American powerhouses of commerce, it is important to recognize that the widespread adoption of modern automation systems – proven in Europe and Asia – does not face the same structural and regulatory hurdles that constrain U.S. ports. This differential in operational flexibility will continue to shape competitive dynamics across the continent’s freight networks

Taken together, these developments signal a fundamental reorientation of North American trade. What began as incremental policy shifts and infrastructure upgrades has now matured into a structural realignment – one where Mexico is no longer a peripheral manufacturing base but a central pillar of the continent’s supply‑chain architecture. This shift sets the stage for the next question: how these new trade patterns are reshaping capacity, costs, and competitive dynamics across the region.

Distribution: The Chicken or the Egg?

As we have established, large‑scale national distribution of consumables and finished goods in the United States relies heavily on imported products. These goods are funneled into national distribution centers – most of which are concentrated near hyper regional population density and coastal markets – where they are sorted and then distributed to retailers and consumers. Depending on the size and sophistication of the organization, this work may be handled through a third‑party logistics provider or through an internally managed distribution network. Major metropolitan areas such as Los Angeles and New York have enough population density and consumption to justify dedicated distribution facilities located in reasonable proximity to their port gateways.

Although distribution is often associated with retail products, it is also a critical component of manufacturing. Only in limited cases does manufacturing function as a single, linear transaction – where a raw material is extracted, processed, packaged, and prepared for market within one integrated complex. Salt production is a good example: mining, processing, packaging, and distribution often occur on the same site, and the commoditized nature of the product makes it cost‑prohibitive to ship it elsewhere for additional processing.

As products become more complex, the sourcing of feedstocks becomes increasingly sophisticated. Electric vehicle manufacturing is a prime example, with inputs and raw materials sourced from around the world. While established automakers such as GM and Stellantis leverage existing factories with billions of dollars in embedded capital, newer brands like Lucid and Tesla assemble vehicles in Casa Grande, Arizona, and Fremont, California. Their locations are not coincidental – they sit near major global supply‑chain gateways, including West Coast ports and robust U.S.–Mexico trade corridors, enabling efficient access to international feedstocks, and manufactured constituent materials.

The first global plant dedicated exclusively to producing Electric Vehicles (EVs) for a major U.S. automaker is Ford’s facility in Cuautitlán Izcalli, Mexico, underscoring Mexico’s growing role as a strategic manufacturing hub within the North American supply chain.

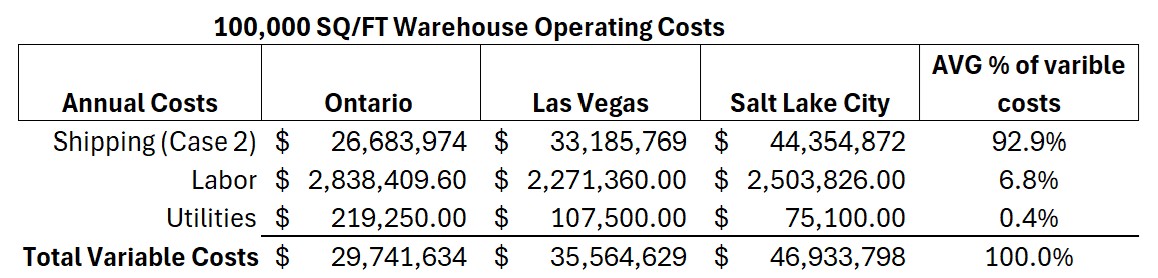

Competitiveness often becomes a direct function of transportation costs. In a recent variable‑cost analysis comparing three markets – Ontario, CA; Salt Lake City, UT; and Chicago, IL- it became clear that when 100% of product is imported, supply‑chain dynamics can outweigh nearly every other cost driver. After conducting a robust origin‑and‑destination freight analysis, it was evident that supply chain considerations are as significant, if not more significant, than real estate costs. In this case, labor for a 50‑person operation accounted for only about 7% of total variable costs, a stark contrast to service‑based industries, while transportation represented more than 92%.

Although supply‑chain pricing is influenced by many factors, it is largely driven by capacity and balance. For example, match‑back volumes from Chicago into Salt Lake City are limited. Even though the mileage is shorter than Ontario, the imbalance influences pricing upward. When a lane becomes constrained, surge pricing emerges as shippers with time‑sensitive or margin‑sensitive freight demonstrate a willingness to pay. This dynamic affects all pricing within the impacted lanes. A dramatic example of this phenomenon was the Shanghai‑to‑Long Beach trade lane during 2021–2022, when extreme imbalance and capacity shortages drove unprecedented rate spikes, proving the vulnerability caused by the relationship between cost and capacity.

Returning to the introductory premise: rather than chasing whatever industry is currently fashionable or promises higher tax revenue, communities should begin by examining their true competitive advantages. What is already moving through the market, and why? How would feedstock or component flow into a targeted facility, and what would outbound distribution look like? Is that flow more competitive than the alternative markets a firm is evaluating? If not, the next question becomes: what appetite exists- politically, financially, and socially – to improve that competitiveness?

In manufacturing, the supply chain is often the decisive factor. Communities must also consider whether securing a specific project justifies the public investment required to make the location viable. A well‑studied example is BMW’s decision in the mid‑1990s to locate U.S. production near the Port of Savannah – a move that catalyzed transformative growth in the region’s logistics ecosystem. In today’s competitive landscape, however, manufacturers are increasingly unwilling to shoulder the substantial upfront infrastructure costs needed to create a competitive supply‑chain environment, particularly when the resulting improvements are not exclusive to them once completed. This exposes a core challenge in post‑performance‑only economic development models: public infrastructure is a major driver of supply‑chain competitiveness, and its economic value is more appropriately measured through regional and sector‑wide impact rather than firm‑specific outcomes.

With this framework in mind, Utah provides a clear example of how communities can evaluate their competitive position. By examining what moves through the state today – and what could move tomorrow – we can better understand where targeted investments would meaningfully shift market dynamics.

From Raw Materials to Advanced Manufacturing: Utah’s Downstream Opportunity

Utah competes nationally in advanced manufacturing, aerospace and defense, software and financial services, life sciences, and natural‑resource‑based industries, but its long‑term competitiveness hinges on strengthening supply chain resilience and expanding downstream value creation. As noted earlier, national distribution from Utah can be challenging depending on origin–destination pairs; however, the state is highly competitive in regional distribution across the Intermountain West.

The state benefits from a central geographic position, a skilled workforce, and a strong defense industrial cluster, yet it faces constraints in rail‑served industrial capacity, cold‑chain and Good Manufacturing Process (GMP) infrastructure – a requirement for pharma, and the depth of its tier‑2 (feedstock) and tier‑3 (raw material) supplier base. Increasing the in‑state conversion of Utah’s raw materials—such as salt, hydrocarbons, minerals, and agricultural outputs – into higher‑value feedstocks and intermediate goods would reduce import dependence, anchor new manufacturing activity, and improve economic resilience.

Targeted investments in industrial land, feedstock‑focused clusters, and energy‑transition materials represent actionable opportunities to close market gaps and position Utah as a more integrated and strategically essential node in national supply chains. Shortening supply chains generates exponential benefits: higher profitability, reduced transportation risk, lower carbon intensity, and a more competitive landscape for consumers and manufacturers. These gains are especially pronounced when raw materials, energy inputs, and logistics capacity are sourced locally.

A copper‑sector example illustrates this opportunity. Today, copper ore extracted at Rio Tinto Kennecott’s Bingham Canyon Mine is processed into concentrate, smelted, and refined into copper cathode – powered in part by Kennecott’s self-generated electricity. From there, while Utah continues to play an important role, a significant portion of additional value creation occurs outside the state, as the cathode is loaded onto rail or truck and the majority is shipped out for further processing.

An alternative scenario illustrates the potential of a shortened, Utah‑based supply chain. Rather than exporting copper cathode, the refined material is delivered to an adjacent facility for production of copper rod, powered by in‑state natural gas from Utah’s net‑exporting energy system. The rod is then drayed by Utah trucking firms or moved by rail to an in‑state wire production facility – an asset the state currently lacks. From there, the wire becomes an essential feedstock for the defense industrial base, supplying firms such as Northrop Grumman, L3Harris, Boeing, and other manufacturers located within an hour of the Wasatch Front.

In this model, Utah closes a critical feedstock gap, matches or exceeds the competitive position of Arizona (the only other U.S. state with an active copper smelter), removes weeks or even months from the supply chain cycle, and strengthens the competitiveness of advanced manufacturing while leveraging in‑state fuels, natural gas, labor, and logistics capacity. The downstream economic effects extend to local service providers, retailers, and small businesses. Though entirely theoretical, this is precisely the type of scenario communities and developers should be evaluating when considering long‑term industrial strategy.

Conclusion: Supply Chains as Strategy in a Changing Economic Landscape

The evolution of America’s supply chains – from ancient logistics principles to modern global networks – reveals a consistent pattern: regions thrive when they align their economic strategies with the realities of how goods move. As this paper has shown, the most competitive markets are those that understand their position within national and global flows and invest accordingly. In today’s economy, where disruptions have exposed the fragility of long, offshore‑dependent networks, supply chains are no longer a background consideration; they are the strategy.

The pandemic era made this unmistakably clear. Lean, globally stretched supply chains buckled under pressure, transportation costs surged, with consumers and producers alike absorbing the consequences. These shocks accelerated a structural shift toward nearshoring, regionalization, and resilience – trends reflected in Mexico’s rise as the United States’ largest import source and the rapid integration of North American rail networks. As freight patterns realign, regions that once relied on legacy advantages must now reassess their competitiveness through a supply‑chain lens.

For communities, this means moving beyond aspirational industry targeting and instead asking more fundamental questions: What already moves through this market? Why? How competitive is this location compared to the alternatives? As this paper notes, manufacturing success depends on whether a region can bring inputs-in and move outputs-out efficiently. If the answer is no, communities must determine whether they have the appetite – politically, financially, and socially – to improve that position.

Utah’s case study illustrates both the challenge and the opportunity. The state possesses enviable strengths: a central geographic position, a skilled workforce, and a robust defense industrial base. Yet it also faces constraints in rail‑served industrial land, cold‑chain and GMP capacity, and the depth of its tier‑2 and tier‑3 supplier ecosystem. Today, much of Utah’s raw material wealth leaves the state for value‑added processing elsewhere, as seen in the copper example where more than 98% of cathode is shipped out of state for further refinement.

But the alternative scenario presented in this paper demonstrates what becomes possible when regions invest in feedstock conversion and supply‑chain integration. In that model, Utah closes a critical feedstock gap, accelerates production cycles, strengthens its advanced manufacturing base, and captures value that currently flows to other states. This is not merely a copper story – it is a blueprint for how communities can transform natural advantages into durable economic engines.

Ultimately, the path forward for any region is clear: competitiveness will belong to those that understand their supply chains, invest in the infrastructure and feedstock capabilities that matter, and build ecosystems where raw materials, energy, logistics, and manufacturing reinforce one another. The opportunity is not simply to attract projects, but to create the conditions that make a region indispensable within the modern economy.

To circle back to the beginning– “Advanced manufacturing refers to the use of innovative technologies to create new products, refine existing products, and perform production activities that will improve the quality and process of manufacturing to give manufacturers a competitive edge.” (Finch, 2024). They differ from traditional manufacturing as they are highly reliant on agility, fully embrace the integration and development of technology – including AI, and continuous press innovation.

Supply chains are the strategy. Regions that embrace this reality will shape their own economic future; those that do not will be shaped by the decisions of others.

About the authors:

Armando Tirado is a supply chain strategist specializing in integrating rail within multimodal logistics, industrial infrastructure, and market‑driven site selection. He advises developers, operators, and public agencies on network design and freight‑centric growth. With more than 20 years of industry experience – including senior operating roles at Class I and Class III railroads and one of North America’s largest privately held 3PLs – he has led and developed every major component of the supply chain.

Kyle Roberts is a senior industrial real estate and supply chain advisor with 30 years of experience guiding manufacturers, logistics operators, and investors through complex site selection, development, and operational decisions. As Vice Chairman of Newmark Mountain West, he serves on Newmark’s National Industrial & Supply Chain Board. His transaction portfolio spans more than 130 million square feet and exceeds $7.2 billion in cumulative value, including many of the market’s largest industrial capital markets deals and most complex build‑to‑suit projects.